Brightline Train Florida: Stations, Fares, Schedule & Expansion Plans 2026

Brightline Florida 2026: $5.5B debt, $233M loss, ‘substantial doubt’ warning, Stuart station blocked, Q1 2026 record ridership (900k+). Tampa extension status & Brightline West update.

⚡ In Brief

🚨 May 2026 Critical Update: Brightline Florida’s latest financial audit (April 30, 2026) raised “substantial doubt” about the company’s ability to continue as a going concern. The company reported a $233 million net loss in 2025, has $5.5 billion in total debt, and has deferred multiple interest payments. While Q1 2026 ridership reached a record 900,000+ passengers, the company lacks sufficient liquidity to meet its obligations. A debt restructuring or Chapter 11 bankruptcy filing is considered likely within months by industry analysts.

When Brightline began South Florida operations in January 2018, connecting Miami to West Palm Beach with a fleet of Siemens trainsets and a hospitality-focused passenger experience, American rail observers watched with cautious interest. Privately financed, privately built, privately operated — the model ran directly against a century of American passenger rail orthodoxy that held intercity rail to be an inherently public-sector activity. Amtrak had existed since 1971 precisely because the private railroads had all concluded that passenger rail was unprofitable and given it up.

Five years later, Brightline had extended 170 miles north to Orlando International Airport for $6 billion, achieved 2.75 million annual passengers, and was planning two further expansions — to Tampa in Florida and to Los Angeles in California. It had also accumulated $4.6 billion in debt, reported a $549 million net loss in 2024, and had its bond credit rating cut to B by Fitch in July 2025. The Brightline story is simultaneously the most encouraging and the most cautionary tale in contemporary American passenger rail. Understanding it requires understanding both what Brightline has achieved and what it has not yet solved.

Project Fact Sheet

| Attribute | Details |

|---|---|

| Project name | Brightline Florida Higher-Speed Rail |

| Operator | Brightline Trains LLC (private; majority owned by Fortress Investment Group) |

| Current operating corridor | Miami – Fort Lauderdale – Boca Raton – West Palm Beach – Aventura – Orlando Airport: 378 km (235 miles) |

| Maximum speed | 200 km/h (125 mph) |

| Journey time Miami–Orlando | ~3 hours 10 minutes |

| Rolling stock | Siemens Charger locomotives + Siemens Venture coaches (diesel-electric, EPA Tier 4) |

| Phase 1 (South Florida) | 104 km; operational since 2018; Miami – West Palm Beach |

| Phase 2 (Orlando extension) | 273 km; $6 billion; opened September 2023 |

| Phase 3 (Tampa extension) | ~137 km; $400M bond financing sought (2025); construction timeline not yet confirmed |

| Annual ridership (2024) | 2.75 million |

| Total debt (2024) | $4.6 billion |

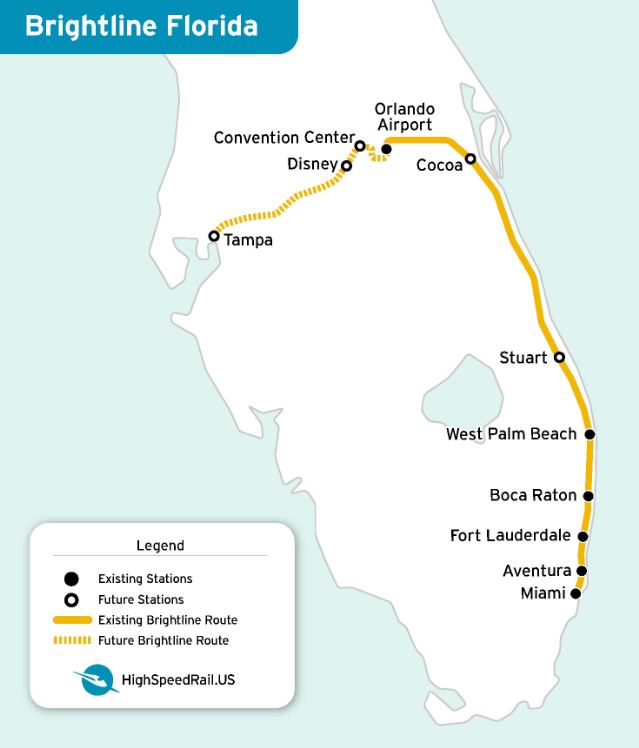

Phase Development: From South Florida to the State

Phase 1: Miami to West Palm Beach (2018)

Brightline launched South Florida operations in January 2018, connecting Miami’s MiamiCentral station to West Palm Beach via Fort Lauderdale. The 104 km route used upgraded alignment along the Florida East Coast Railway (FECR) corridor — a privately owned freight railroad that provided the right-of-way for Brightline’s operations. Stations in Aventura and Boca Raton were added in 2022, completing the initial South Florida network at six stations.

Phase 1 demonstrated the viability of the hospitality-oriented model: departure lounges at stations, complimentary food and beverage in PREMIUM class, Starlink high-speed internet on board, and a consistent on-time performance that compared favourably with the competing I-95 highway corridor. South Florida commuter demand proved real, with regular users adopting passes for the Miami–West Palm Beach journey.

Phase 2: West Palm Beach to Orlando International Airport (2023)

The Phase 2 extension — 273 km from West Palm Beach to Orlando International Airport — was the transformative and most expensive element of the project. The $6 billion construction began in 2019 and required building an entirely new dedicated passenger railway alignment for the central Florida segment, including:

- Major new viaduct and bridge structures, including reconstruction of the St. Lucie and Loxahatchee River bridges.

- 156 grade crossing upgrades along the FECR corridor to meet FRA requirements for 200 km/h passenger operations alongside freight.

- A new 4.8 km elevated guideway into Orlando International Airport’s intermodal terminal.

- The Orlando Airport station, directly integrated with the airport’s Terminal C and the SunRail commuter rail connection.

Service launched September 2023. As of September 2025, Brightline operates 8-coach train formations during peak periods (growing to 10-coach by end of 2025), with 28 daily departures from Boca Raton — up from 19 — and peak/off-peak pricing introduced for South Florida trips.

Phase 3: Tampa Extension – Status (May 2026)

The proposed Phase 3 extension — approximately 137 km (85 miles) from Orlando to Tampa along the I-4 highway median — would complete the Florida megaregion corridor and create a one-hour Tampa-Orlando journey time. As of May 2026:

- Brightline continues seeking $400 million in tax-exempt bonds through the Florida Development Finance Corporation (FDFC) to fund design and initial construction

- Tampa’s city board voted unanimously in July 2025 to allow Brightline to continue FDFC bond negotiations

- However, the timeline remains highly uncertain due to Brightline’s deepening financial crisis. A former Brightline executive has estimated the extension could take another 10 years to complete

- No state or federal government funding has been committed as of May 2026

- Proposed intermediate stations include Lakeland, Disney/International Drive area, and Downtown Tampa

The I-4 highway itself is undergoing a major expansion project expected to take 15–20 years, though state officials may accelerate that timeline. It would make sense for Brightline to lay tracks concurrently with highway construction, but the company’s ability to raise the necessary capital is now in serious question.

📉 Record Ridership: Why Growth Isn’t Enough

Ironically, Brightline is carrying more passengers than ever before. In the first quarter of 2026, the company carried more than 900,000 passengers — the highest quarterly number ever — and reported a record $61.2 million in revenue, up 12% from Q1 2025. March 2026 was the company’s best month ever, with 337,874 riders (up 21% year-over-year) and $23.6 million in revenue.

However, ridership still falls far short of original projections. In 2025, its second full year of service to Central Florida, Brightline carried just 3.1 million passengers (a 13% increase from 2024) and took in $214 million in revenue — far below the 6.6 million passengers and $697 million in annual revenue originally projected.

The fundamental problem is that it cost Brightline $282 million to operate its trains and stations in 2025, plus $59 million in corporate and administrative expenses, for a total operating loss of $127 million. Add $114 million in interest payments, and the company was $233 million in the red. Even with record ridership, the math simply doesn’t work — yet.

Average fares tell the story: South Florida passengers paid $26.72 per ride in Q1 2026 (down from $30.40), while Orlando passengers paid $78.85 (up slightly from $74.26). To reach break-even, analysts estimate Brightline needs approximately 5–6 million annual passengers — roughly double current volumes.

Rolling Stock: Siemens Charger + Venture

| Component | Specification |

|---|---|

| Locomotive | Siemens Charger SC-44 diesel-electric; 2 per trainset |

| Engine | Cummins QSK95 diesel; 4,000 hp per locomotive; EPA Tier 4 certified |

| Coaches | Siemens Venture stainless-steel coaches; designed by Rockwell Group |

| Train formation | Currently 8-coach peak; expanding to 10-coach; push-pull operation |

| Maximum speed | 200 km/h (125 mph) |

| Boarding | Level boarding via automated retractable platforms |

| Connectivity | Starlink satellite internet; power outlets at all seats |

| Emissions | EPA Tier 4 (low NOx, low particulate); ~75% lower NOx than Tier 0 |

Brightline has ordered 30 additional Siemens Venture coaches to accommodate growth on the existing corridor and potential Phase 3 operations. The trainsets‘ diesel-electric traction reflects the absence of electrification on the FECR corridor — a deliberate design choice that reduced Phase 2 capital costs but limits top speed compared to a true electrified high-speed railway.

Financial Position: The Central Challenge

Brightline’s financial performance through 2024 illustrates the structural tension in the private passenger rail model:

| Metric | 2024 | Context |

|---|---|---|

| Annual ridership | 2.75 million | +700,000 vs 2023; growth trajectory positive |

| Revenue | $188 million | Average yield: ~$68 per trip |

| Operating costs | $341 million | Operating ratio ~181% (spending $1.81 for every $1.00 earned) |

| Interest payments | $178 million | Debt refinanced to $4.6 billion total in 2024 |

| Net loss | $549 million | Ridership would need to roughly double to reach break-even |

| Bond credit rating | B (Fitch, July 2025 — downgraded from BB+) | Deferred July 2025 interest payment on unrated bonds |

The financial picture reflects a system in the early, high-cost stage of its lifecycle: $6 billion of Phase 2 capital costs are being serviced at current interest rates while ridership is still building toward the levels needed to support the debt. Comparable international intercity rail launches — the Channel Tunnel, Eurostar, HS1 in the UK — all required 10–15 years of post-opening losses before achieving sustainable financial performance, and all ultimately required some form of debt restructuring.

🚨 2026 Financial Crisis: “Substantial Doubt” & Going Concern Warning

On April 30, 2026, Brightline Florida released its audited annual financial statement, prepared by Ernst & Young. The report included a stark warning: “substantial doubt exists about the company’s ability to continue as a going concern.” The company acknowledged that it does not currently have the liquid funds necessary to repay its indebtedness and meet other obligations as they come due.

Key financial metrics from the 2025 report:

- Net loss: $233.1 million (improved from $548.7 million in 2024)

- Operating loss: $127 million

- Total debt: Approximately $5.5 billion (other sources estimate up to $6.3 billion across various bonds)

- Cash on hand (as of Jan. 1, 2026): Just $1.37 million in unrestricted cash, versus $120 million in accounts payable

- Annual interest payments: ~$115 million, with over $2.5 billion in total interest due over the next two decades

Fitch Ratings downgraded Brightline’s senior bonds to “CCC” in January 2026, reflecting “substantial credit risk” and elevated default risk by the first half of 2027. The company has also deferred multiple interest payments, including a $117 million payment originally due February 17, 2026, which has been pushed to June 15, 2026.

🛑 Stuart Station: FEC Blocks Treasure Coast Stop

In May 2026, plans to build a Brightline station in Stuart suffered a major setback. Florida East Coast Railway (FEC), which owns the rail corridor Brightline operates on, formally denied approval for the proposed station. In a letter dated April 27, 2026, FEC’s senior vice president stated that the company cannot support “any station” because it would result in the existing Stuart bridge violating U.S. Coast Guard rules.

The proposed station, estimated to cost up to $60 million, was required under a 2018 settlement with Martin County, which stipulated that Brightline must build a Treasure Coast station within five years of launching Orlando service (which began September 22, 2023). Martin County and the city of Stuart had offered to pay approximately 75% of the construction cost.

Stuart’s mayor declared the project “dead right now,” though Brightline has pushed back, stating the objections “lack merit” and that the company “remains committed” to the station. However, without FEC’s express written approval, Brightline cannot unilaterally build anything on the corridor. The station’s future is now highly uncertain.

💸 Bankruptcy Watch: What Comes Next?

Industry analysts and restructuring experts widely agree that a debt restructuring — whether in or out of court — is coming within months. Brightline has hired Skadden Arps as legal counsel and is actively negotiating with creditors. The company’s complex debt structure includes:

- $2.2 billion in tax-exempt senior bonds (Opco bonds), with $1.1 billion guaranteed by Assured Guaranty

- $1.2 billion in unrated subordinate bonds (Holdco bonds)

- Multiple creditor factions, including Invesco, Nuveen, First Eagle Investments, and distressed specialists Redwood Capital, Aristeia Capital, and Nut Tree Capital

In a bankruptcy scenario, the most likely outcome is a Chapter 11 restructuring rather than liquidation — the physical railway infrastructure (track, stations, rolling stock) has substantial value, and the operating business is growing. A restructuring would likely involve debt-for-equity conversion, reducing the interest burden that is the primary driver of current losses.

Fortress Investment Group, Brightline’s majority owner, has already lost an estimated $2.2 billion in equity over more than a decade and may be preparing to relinquish control. Several deep-pocketed infrastructure funds and strategic buyers are reportedly circling as potential investors or acquirers.

Brightline West: Las Vegas to Southern California

Brightline West is a separate entity from Brightline Florida — it is a distinct company, on a distinct route, using a completely different technology. Where Brightline Florida is a higher-speed diesel-electric railway at 200 km/h, Brightline West is a true high-speed railway targeting 320 km/h (200 mph) on an electrified dedicated alignment along the I-15 freeway median from Las Vegas to Rancho Cucamonga in Southern California.

- Distance: ~275 km (171 miles)

- Target speed: 320 km/h (200 mph)

- Journey time: ~2 hours Las Vegas to Rancho Cucamonga (Metrolink connection to Los Angeles)

- Estimated cost: $12 billion total

- Federal funding: $3 billion committed by Biden administration (2024)

- Target opening: Before 2028 Los Angeles Olympics

- Technology: Electrified HSR on dedicated right-of-way; rolling stock not yet confirmed

Brightline Florida vs True High-Speed Rail

| Attribute | Details (May 2026) |

|---|---|

| Project name | Brightline Florida Higher-Speed Rail |

| Operator | Brightline Trains LLC (private; majority owned by Fortress Investment Group) |

| Current operating corridor | Miami – Fort Lauderdale – Boca Raton – West Palm Beach – Aventura – Orlando Airport: 378 km (235 miles) |

| Maximum speed | 200 km/h (125 mph) |

| Journey time Miami–Orlando | ~3 hours 10 minutes |

| Annual ridership (2025) | 3.1 million |

| Q1 2026 ridership | 900,000+ (record) |

| Total debt (2025/2026) | $5.5–6.3 billion |

| Net loss (2025) | $233 million |

| Fitch credit rating (Jan 2026) | CCC (substantial credit risk) |

| Phase 3 Tampa extension | ~137 km; $400M bond financing sought; timeline highly uncertain |

| Brightline West cost | $21.5 billion (up from $12 billion) |

| Brightline West target opening | Late 2029 (pushed from 2027) |

Editor’s Analysis

Brightline’s position in early 2026 is genuinely ambiguous — not failing, not succeeding, but suspended at the inflection point between an unproven experiment and a sustainable operation. The ridership trajectory is real: 2.75 million annual passengers in 2024, growing meaningfully year-on-year, represents a genuine market that did not exist before Brightline created it. The financial trajectory is also real: $549 million net loss, $4.6 billion in debt, a deferred bond payment in July 2025, and a Fitch downgrade that reflects genuine investor concern about whether ridership can grow fast enough to service the debt load. The critical question is whether Brightline can reach the 5–6 million annual passenger level — roughly double current volumes — at which operating costs and interest can be covered from fare revenue. That level is plausible on the Miami–Orlando corridor if the Orlando tourism market fully converts to rail, but it requires years of continued growth without a financial crisis that forces debt restructuring or reduces service quality. The Phase 3 Tampa extension is both a strategic opportunity and a financial risk — it adds a corridor that could materially increase total system ridership (Tampa Bay is Florida’s third-largest metro, and the Tampa–Orlando city pair is precisely the 100-mile distance where rail is most competitive with driving) but requires capital that the company does not currently have and cannot easily raise at its current credit rating. The story of whether private passenger rail in the United States is viable will largely be written by whether Brightline reaches profitability before its creditors run out of patience. — Railway News Editorial

Frequently Asked Questions

- Q: Is Brightline actually “high-speed rail”?

- Brightline Florida is technically classified as “higher-speed rail” rather than true high-speed rail (HSR). The UIC definition of high-speed rail requires a maximum operating speed of at least 250 km/h on purpose-built infrastructure. Brightline Florida operates at a maximum of 200 km/h (125 mph) on a mixture of upgraded existing FECR freight corridor and new dedicated alignment — below the 250 km/h HSR threshold. Brightline’s own marketing uses “higher-speed rail” or “premium intercity rail.” Brightline West (Las Vegas to Southern California), targeting 320 km/h on a dedicated electrified alignment, will meet the HSR definition when complete.

- Q: Why is the Miami–Orlando journey 3+ hours if the train goes 125 mph?

- The 3-hour-plus Miami–Orlando journey reflects several factors that prevent the full 200 km/h speed from being sustained for the entire trip. First, the route has six intermediate station stops, each requiring deceleration and acceleration. Second, on the South Florida segment (Miami to West Palm Beach), the train shares the FECR corridor with freight traffic and runs through densely populated areas with 156 grade crossings, requiring speed restrictions below maximum. Third, curve geometry and grade crossing safety limits constrain speed on portions of the route. Average commercial speed — the distance divided by total trip time — is approximately 120 km/h, which is typical for higher-speed intercity rail with intermediate stops. For comparison, driving the I-95/Florida Turnpike route takes approximately 3–3.5 hours without traffic.

- Q: What is the current status of the Phase 3 Tampa extension?

- As of early 2026, Phase 3 remains in the financing and preliminary engineering stage. Brightline is seeking $400 million in tax-exempt bonds through the Florida Development Finance Corporation to fund the design and initial construction of the Orlando–Tampa segment, proposed to run along the I-4 highway median. Tampa City Board voted unanimously in July 2025 to authorise continued bond negotiations. However, no construction start date has been announced, no state or federal funding has been committed, and the station location study for Tampa is still underway. The Phase 3 timeline is also complicated by Brightline’s financial position — the company deferred a bond interest payment in July 2025, which may affect its ability to raise new capital for expansion.

- Q: How does Brightline compare to Amtrak’s Auto Train and other Florida rail services?

- Brightline and Amtrak serve different markets with different service models in Florida. Amtrak operates the Auto Train (Lorton, Virginia to Sanford, Florida — a car-carrier train) and the Silver Service/Palmetto routes connecting Miami to the Northeast via the Seaboard Coast Line corridor on the west side of the state. Brightline operates on the Florida East Coast corridor on the east side, with a premium hospitality-oriented product at frequency (up to 16 Miami–Orlando round trips daily) that Amtrak cannot match. SunRail is the Central Florida commuter rail service, operating around Orlando on a different alignment and connecting to Brightline at the Orlando Airport station. Brightline’s fares (averaging $70 one-way Miami to Orlando) are significantly higher than Amtrak’s equivalent journey but offer better frequency, on-time performance, and station facilities.

- Q: What happens to Brightline’s Florida operations if it goes bankrupt?

- Financial analysts and railway observers have discussed this scenario given Brightline’s $4.6 billion debt load and continuing losses. In a bankruptcy scenario, the most likely outcome is a Chapter 11 restructuring rather than liquidation — the physical railway infrastructure (track, stations, rolling stock) has substantial value and the operating business is growing, making it a viable restructuring candidate rather than a closure candidate. The FECR freight railway that Brightline partly shares would continue operating regardless of Brightline’s financial position. A restructuring would likely involve debt-for-equity conversion, reducing the interest burden that is the primary driver of current losses. Several comparable intercity rail projects internationally — Eurostar, the Channel Tunnel — underwent financial restructuring in their early years without service interruption, eventually achieving stable operation. Florida state intervention to take over operations is also possible if closure was threatened, given the system’s economic importance to the Orlando tourism corridor.

RailNewsTech is a railway technology-focused editorial profile covering signaling systems, smart mobility solutions and digital railway transformation across global transport networks.

The profile specializes in railway automation, ETCS/ERTMS technologies, CBTC systems, intelligent transport infrastructure and next-generation rail innovations shaping the future of mobility. Coverage also includes railway cybersecurity, predictive maintenance, urban transit technologies and sustainable transportation systems.

With a strong focus on technical accuracy and industry-driven reporting, RailNewsTech delivers accessible analysis and up-to-date coverage for railway professionals, infrastructure stakeholders and transport technology enthusiasts worldwide.

RELATED POSTS

July 1, 2026 6:37 am

Amtrak launched a small-plate dining program for Acela First Class...

July 1, 2026 8:49 am

The Short Line Training Center launched FRA-funded online DSLE and...

BART secured the non-monetary GFOA Triple Crown Award for fiscal...

July 5, 2026 9:19 am

APTA named 10 US public transit agencies as winners of...

July 9, 2026 11:10 pm

California HSR signed a 30-month deal with Keolis and SNCF...

July 12, 2026 3:12 am

Amtrak launched 13 NextGen Acela trainsets on the Northeast Corridor...